AI: Trojan Horse or Growth Engine?

While stocks on the forefront of developing AI chips and applications have had outsized returns over recent years, investors are now questioning if the benefits will outweigh the spending. Furthermore, many IT companies that initially saw AI as an opportunity now realise that AI can be a threat to their business models. Recent volatility suggests AI may be a Trojan Horse to the broader IT sector.

The last few years of stock market investing has been dominated by the ‘Magnificent 7’, seven dominant, large-cap technology companies that significantly influence the US stock market and major indices like the S&P 500 and the Nasdaq. They are primarily recognised for their leadership in AI, cloud computing, and digital services.

The rise of these stocks has led many to believe that if AI is the future of technology, then surely IT stocks will outperform more traditional companies. Certainly, AI has given a boost to IT stocks, driving prices to record highs in recent years. But since October last year, that exuberance has been fading as some realities of this transformative technology have begun to sink in.

Investors are now questioning the amount of money that companies are spending on AI, and whether the benefits will be worth it. In early February, Amazon revealed that it planned to spend $US200 billion on AI this year, while Google’s parent Alphabet said it would spend as much as $US185 billion. Meta said its capital expenses, in large part to support AI, could reach $US135 billion.

But another catalyst for the sell-off was the release in February by artificial intelligence firm Anthropic of free plug-in software tools that allow companies to automate functions like customer support and legal services.

Furthermore, free software models from AI companies have the potential to replace not only the business models of software-as-a-service (SaaS) companies, but also much of the workforce employed by them. For example, shares of Salesforce, which produces SaaS and customer relationship management software for sales workers, have fallen 25% over the past month.

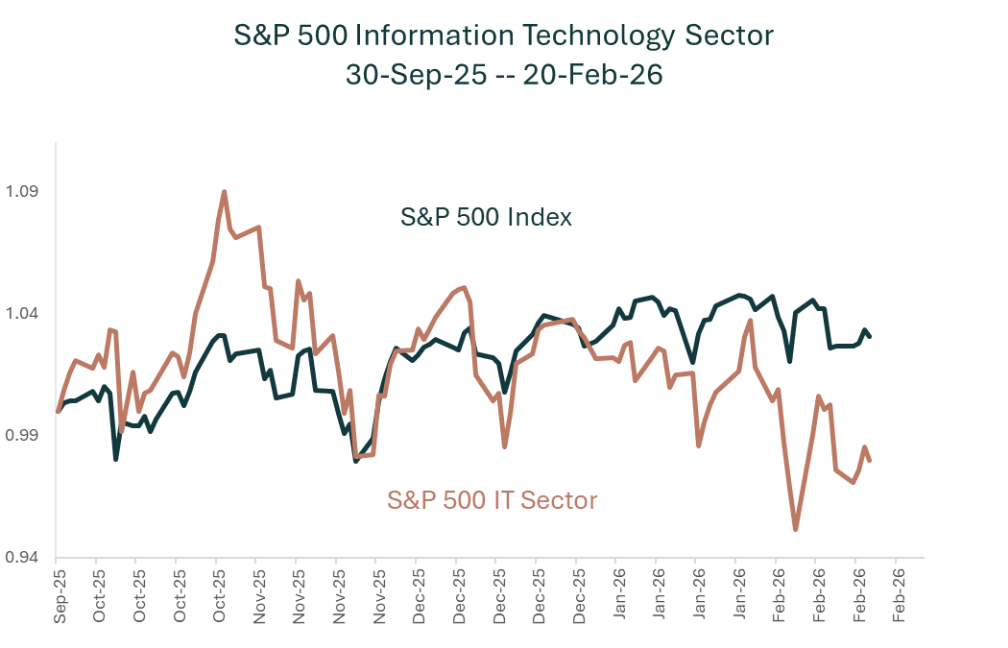

The chart below shows the short-term trading behaviour of the S&P 500 Index and the Information Technology Sector. Since the end of September, the broad market is up 3.8% (in USD), while the IT Sector is down 2%. This negative return has a significant impact on the broad market, as the IT Sector constitutes just over the 30% by market cap of the S&P 500 Index. The bump in the IT Sector at the start of November was based on expectations of the Federal Reserve cutting rates.

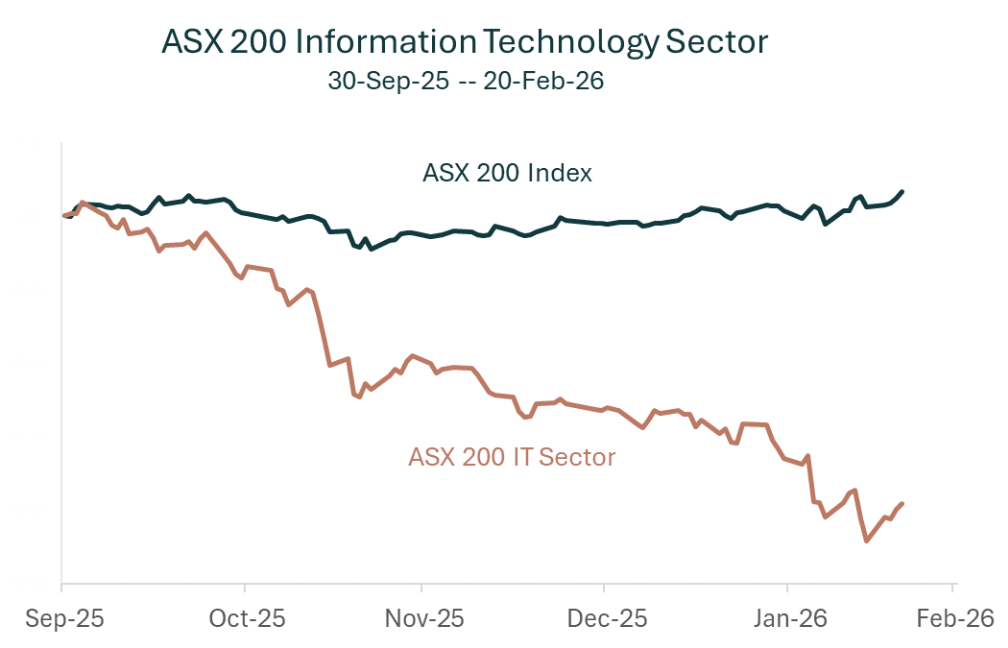

The chart below shows the fall in value of the local ASX 200 Information Technology Sector relative to the broader ASX 200 Index. It’s been a tech wreck for the local IT Sector. The local market is up 3.4% since the end of September, but the IT Sector is down over 40%. This has little effect in a diversified portfolio, as the IT Sector is only around 3% by market value of the broad market.

The fall in the Australian IT Sector started in November. Just the US IT Sector jumped on the possibility that interest rates would be cut by 50 bps, the local market had to contend with a much higher than expected inflation print, leading the bond market to instantly price an increase in the Australian cash rate at the next meeting of the RBA.

The issues in Australia are less about the concerns on how much capex is being spent on AI, but more about the impact of AI disruption on software players. Local IT giant Atlassian Corporation – which has its headquarters in Sydney but is listed on the Nasdaq in the US – was down 10% with other Software-as-a-Service companies.

In the local IT Sector, the big names are REA Group (digital advertising and real estate), WiseTech Global (SaaS logistics software) and Xero Ltd (cloud accounting software), which are all down between 30% and 50% since the end of September last year.

But there may be other collateral damage from the fall in tech stocks, such as in private credit and private equity, where exposure to the software sector is estimated at about 20%. Software companies have been a favourite target of lenders of private credit, because the companies’ subscription-based business model provides a stable stream of income to support taking on more debt.

AI is clearly a disruptor, not only for stocks but for society as well. It is increasingly viewed as a ‘Trojan Horse’ because its appealing, high productivity promise often hides significant, long-term risks5. But it is also a Trojan Horse to the IT sector, because many IT companies have sought to capitalise on the potential of AI, only to find it is challenging their existing business models.

The recent volatility in the IT Sector is part and parcel of investing in the stock market. The most effective strategy for managing sector volatility is diversification. By spreading investments across various sectors, asset classes, and geographies, investors can ensure that the poor performance of one sector is offset by the better performance of another.

Please contact us on +61 3 9935 0970 or email admin@warrhunt.com.au if we can be of assistance.